2026 HSA Limits: Maximize Tax-Advantaged Contributions

Anúncios

The 2026 Health Savings Account (HSA) limits are essential for individuals seeking to optimize their tax-advantaged healthcare savings and strategically manage future medical expenses.

Anúncios

Understanding the 2026 Health Savings Account (HSA) Limits: Maximizing Your Tax-Advantaged Contributions is more critical than ever for individuals and families navigating the complexities of healthcare costs in the United States. HSAs offer a unique blend of tax benefits, serving as a powerful tool for both current medical expenses and long-term financial planning. This guide will delve into the specifics of the 2026 limits, explore strategies for maximizing your contributions, and highlight the manifold advantages of utilizing these accounts effectively.

Understanding the 2026 HSA Landscape

The Health Savings Account (HSA) has long been lauded as a powerful financial tool, offering a triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. As we approach 2026, the Internal Revenue Service (IRS) will release updated limits for these accounts, reflecting inflation and other economic factors. These adjustments are crucial for individuals and families planning their healthcare and retirement savings strategies.

Staying informed about the latest HSA limits is not merely a matter of compliance; it’s a strategic necessity. These limits dictate how much you can contribute annually, directly impacting your potential tax savings and the growth of your healthcare nest egg. Proactive understanding allows for better financial forecasting and optimization of your benefits.

What are the Key Changes Expected?

While the definitive 2026 HSA limits are typically announced later in the year, historical trends suggest a continued upward adjustment. These changes usually encompass both individual and family contribution maximums, as well as the out-of-pocket maximums for High-Deductible Health Plans (HDHPs) that qualify for HSA eligibility. It is vital to monitor official IRS announcements to ensure your contribution strategy aligns with the most current figures.

- Individual Contribution Limit: This is the maximum amount an individual can contribute to their HSA for the year.

- Family Contribution Limit: Applies to those with family HDHP coverage, allowing for a higher contribution ceiling.

- Catch-up Contributions: Individuals aged 55 and older can contribute an additional amount, offering a significant boost to their savings as retirement approaches.

- HDHP Deductible Minimums: The minimum deductible an HDHP must have to qualify for HSA eligibility.

- HDHP Out-of-Pocket Maximums: The maximum amount an individual or family can pay out-of-pocket for covered services under an HDHP.

These limits are designed to keep pace with rising healthcare costs, ensuring that HSAs remain a relevant and effective savings vehicle. Properly leveraging these limits can lead to substantial long-term financial benefits.

In essence, the 2026 HSA landscape will continue to offer robust opportunities for saving on healthcare. By staying current with the updated limits, individuals can ensure they are maximizing their contributions and fully harnessing the tax-advantaged growth these accounts provide for future medical needs.

Eligibility Requirements for 2026 HSAs

Before you can even consider maximizing your contributions, understanding the eligibility criteria for a Health Savings Account in 2026 is paramount. HSAs are not universally available; they are specifically tied to enrollment in a High-Deductible Health Plan (HDHP). This fundamental requirement ensures that HSAs are utilized by individuals who bear a greater initial financial responsibility for their healthcare.

The IRS sets specific criteria for what constitutes an HDHP. These plans must meet minimum deductible thresholds and maximum out-of-pocket limits. Failing to meet these requirements means your health plan does not qualify, and you cannot contribute to an HSA, regardless of your intentions to save.

Defining a Qualifying High-Deductible Health Plan (HDHP)

For 2026, the specific deductible minimums and out-of-pocket maximums for HDHPs will be crucial. Historically, these figures have seen slight increases each year to account for inflation. It’s important to verify the exact numbers when they are released by the IRS to confirm your plan’s eligibility.

- Minimum Deductible: Your health plan must have a deductible of at least a certain amount for individual coverage and a higher amount for family coverage.

- Maximum Out-of-Pocket: The total amount you pay for covered medical services (deductibles, copayments, coinsurance) cannot exceed a specific limit for individual or family coverage. Premiums are not included in this calculation.

Beyond the HDHP requirement, there are other essential eligibility rules. You cannot be enrolled in Medicare, nor can you be claimed as a dependent on someone else’s tax return. If you have other health coverage that is not an HDHP, such as a spouse’s plan that covers you and is not an HDHP, you might also be ineligible, with some exceptions for limited-purpose coverage like dental or vision.

Ensuring you meet all eligibility criteria is the first step toward leveraging the benefits of an HSA. A thorough review of your health plan’s specifics against the 2026 IRS guidelines will confirm your ability to contribute and enjoy the associated tax advantages.

Maximizing Your 2026 HSA Contributions

Once eligibility is confirmed, the next crucial step is to develop a strategy for maximizing your contributions to fully capitalize on the tax advantages offered by HSAs. Simply contributing a small amount may not unlock the full potential of these powerful savings vehicles. The goal should be to contribute as much as the 2026 HSA limits allow, especially if your financial situation permits.

Anúncios

Many individuals overlook the long-term growth potential of an HSA. Unlike a flexible spending account (FSA), HSA funds roll over year after year, accumulating over time. This makes it an ideal long-term investment vehicle for future healthcare expenses, particularly in retirement.

Strategies for Full Contribution

Achieving the maximum contribution can seem daunting, but breaking it down into manageable steps can help. Consider setting up automatic contributions from your paycheck if your employer offers this option. This “set it and forget it” approach ensures consistent contributions throughout the year.

- Automate Contributions: Set up regular, automatic transfers from your bank account or payroll deductions to your HSA to ensure you hit the annual maximum.

- Lump-Sum Contributions: If you receive a bonus or tax refund, consider contributing a portion or all of it to your HSA as a lump sum to reach your limit faster.

- Catch-up Contributions: If you are 55 or older, remember to take advantage of the additional catch-up contribution. This can significantly boost your savings in the years leading up to retirement.

- Spousal Contributions: If both spouses are HSA-eligible, each can open and contribute to their own HSA, potentially doubling the family’s overall savings capacity (though family HDHP coverage has a single family limit).

Beyond simply contributing, consider investing your HSA funds. Many HSA providers offer investment options, allowing your money to grow tax-free over time. This can turn your HSA into a powerful retirement savings account, specifically earmarked for medical expenses.

Maximizing your 2026 HSA contributions requires a deliberate approach. By utilizing automation, considering lump-sum deposits, leveraging catch-up provisions, and exploring investment opportunities, you can ensure your HSA works as hard as possible for your financial future.

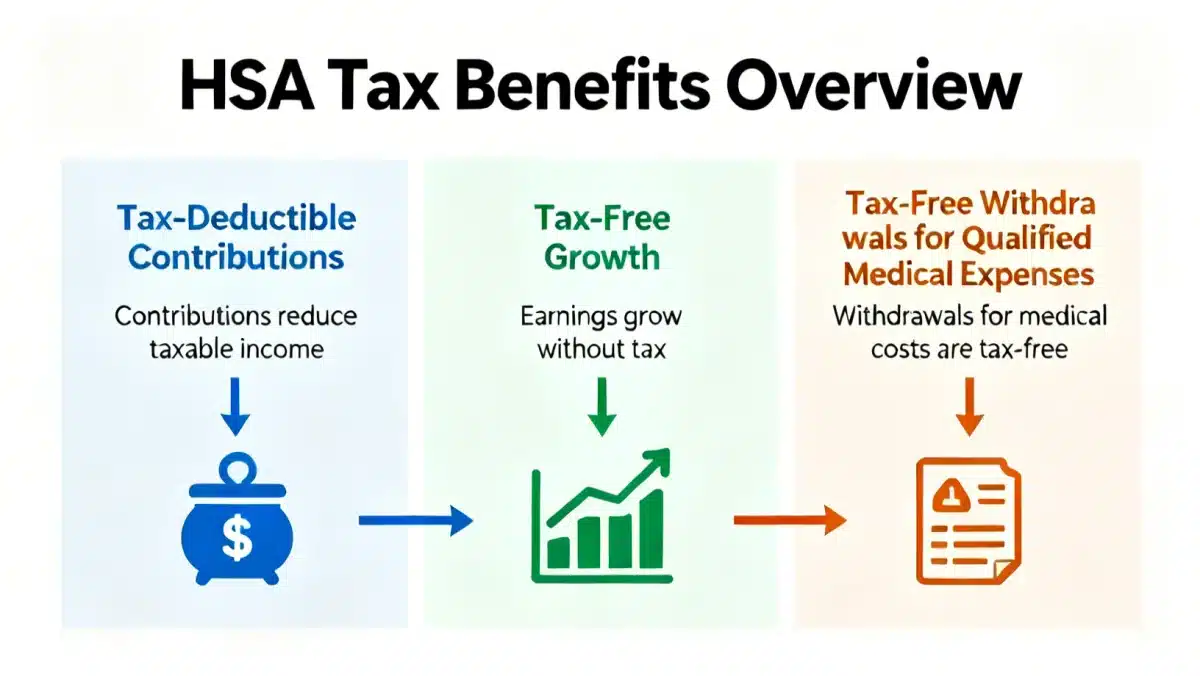

The Triple Tax Advantage of HSAs

The allure of the Health Savings Account lies in its unparalleled triple tax advantage, a benefit rarely found in other investment or savings vehicles. Understanding these three distinct tax breaks is key to appreciating the true financial power of an HSA and why maximizing your 2026 contributions is a strategic move for long-term financial health.

These tax benefits combine to create a highly efficient savings mechanism, not just for immediate medical costs but also for future healthcare needs, particularly in retirement. For many, an HSA can even serve as a supplementary retirement account, offering more flexibility for medical expenses than a traditional 401(k) or IRA.

The first advantage is that contributions to an HSA are tax-deductible. This means that the money you put into your HSA reduces your taxable income, potentially lowering your overall tax bill for the year. This deduction is available whether you itemize or take the standard deduction, making it accessible to a wide range of taxpayers.

The second advantage is tax-free growth. Any earnings on the money invested within your HSA, whether from interest, dividends, or capital gains, grow completely tax-free. This allows your savings to compound more rapidly over time, significantly increasing the potential balance available for future medical expenses.

Finally, and perhaps most compellingly, qualified withdrawals from your HSA are entirely tax-free. When you use your HSA funds to pay for eligible medical expenses, you don’t pay a dime in taxes on those withdrawals. This makes the HSA an incredibly efficient way to cover healthcare costs, from deductibles and co-pays to prescription medications and even some long-term care insurance premiums.

The triple tax advantage of HSAs makes them an indispensable tool for financial planning. By contributing up to the 2026 limits and allowing your funds to grow, you can significantly reduce your tax burden while building a robust reserve for healthcare expenses, both now and in retirement.

Strategic Uses of HSA Funds Beyond Immediate Care

While Health Savings Accounts are primarily designed to help individuals pay for current qualified medical expenses, their unique structure and triple tax advantage make them incredibly versatile for long-term financial planning. Many savvy investors and financial planners view HSAs as a powerful retirement savings vehicle, particularly for healthcare costs in later life, which often represent a significant expense for retirees.

The ability to invest HSA funds and let them grow tax-free, coupled with tax-free withdrawals for qualified medical expenses, positions the HSA as a super-charged retirement account for healthcare. This strategic approach allows individuals to leverage the account’s benefits far beyond typical short-term medical needs.

Investing for Future Healthcare Needs

Instead of using HSA funds for every minor medical expense, consider paying for routine costs out-of-pocket (if financially feasible) and allowing your HSA balance to grow. This strategy, often referred to as “invest and reimburse,” allows your initial contributions to compound over decades. You can save your receipts for qualified medical expenses and reimburse yourself tax-free from your HSA at any point in the future, even years or decades later.

- Retirement Healthcare Costs: Medical expenses are a major concern in retirement. An HSA provides a dedicated, tax-free fund to cover these costs, from Medicare premiums to prescription drugs and long-term care.

- Long-Term Care Insurance: In some cases, HSA funds can be used to pay for qualified long-term care insurance premiums, offering another layer of financial security for the future.

- Dental and Vision Care: Beyond major medical, HSAs can cover a wide range of expenses including dental work, orthodontics, vision care, and even certain over-the-counter medications.

- After Age 65 Flexibility: Once you reach age 65, HSA funds can be withdrawn for any purpose without penalty, though non-qualified withdrawals will be subject to ordinary income tax, similar to a traditional IRA. This provides an additional layer of flexibility in retirement.

By strategically managing your HSA, prioritizing investment, and understanding its various long-term applications, you can transform it from a simple savings account into a cornerstone of your retirement and healthcare financial plan. Maximizing your 2026 HSA contributions is an investment in your future well-being and financial security.

Common Pitfalls to Avoid with HSAs in 2026

While Health Savings Accounts offer significant benefits, it’s crucial to be aware of common pitfalls that can diminish their advantages or even lead to penalties. Navigating the rules and regulations surrounding HSAs requires careful attention to detail, especially concerning eligibility and qualified expenses. Avoiding these missteps ensures you fully reap the rewards of your tax-advantaged contributions in 2026.

One of the most frequent errors is contributing to an HSA when not eligible. This can happen if your health plan no longer qualifies as an HDHP, or if you enroll in Medicare. Ineligible contributions can result in a 6% excise tax, which can quickly erode your savings.

Key Mistakes to Sidestep

Understanding and adhering to the specific guidelines will protect your HSA’s tax-advantaged status. Here are some critical points to remember:

- Ineligible Contributions: Always ensure you are covered by an HDHP and meet all other eligibility requirements before making contributions. Review your health plan annually.

- Non-Qualified Withdrawals: Using HSA funds for expenses that are not considered “qualified medical expenses” before age 65 will result in ordinary income tax and a 20% penalty. After 65, non-qualified withdrawals are only subject to income tax.

- Over-Contributing: While the goal is to maximize, accidentally exceeding the annual contribution limits (individual, family, or catch-up) can lead to penalties. Be meticulous in tracking your contributions.

- Not Investing Funds: A significant missed opportunity is leaving HSA funds in a low-interest savings account. Not investing means missing out on the tax-free growth potential, which is a core benefit of the account.

- Mismanaging Documentation: Although you don’t submit receipts with your tax return, it’s vital to keep detailed records of all qualified medical expenses for which you use HSA funds. This documentation is essential in case of an IRS audit.

Another common mistake is not understanding the interplay between an HSA and other health coverage options. For instance, if your spouse has a non-HDHP plan that covers you, you might be ineligible to contribute to an HSA, even if your own plan is an HDHP. Always check the specifics of all health coverage you and your family hold.

By being diligent about eligibility, understanding qualified expenses, and actively managing your account, you can confidently navigate the complexities of HSAs and fully leverage their benefits for your financial well-being in 2026 and beyond.

Future Outlook and Evolution of HSAs

The Health Savings Account has evolved significantly since its inception, adapting to changes in healthcare policy and economic realities. As we look towards 2026 and beyond, the role of HSAs in personal finance and healthcare strategy is likely to continue its dynamic trajectory. Understanding the potential future outlook can help individuals make more informed decisions about their long-term financial planning.

There is ongoing discussion and debate surrounding healthcare policy in the United States, which could influence the future of HSAs. While the core structure of HSAs has remained stable, minor adjustments to eligibility, contribution limits, or qualified expenses are always a possibility depending on legislative priorities.

Potential Legislative Changes and Their Impact

Historically, both Democratic and Republican administrations have recognized the value of HSAs, albeit with different perspectives on their application and scope. Future legislative changes could focus on expanding HSA eligibility to a broader range of health plans, increasing contribution limits more aggressively, or even introducing new types of qualified expenses.

- Expanded Eligibility: There have been proposals to allow more individuals to contribute to HSAs, even if they don’t have a traditional HDHP, potentially including those with certain chronic conditions or Medicare beneficiaries.

- Increased Flexibility: Discussions around allowing HSA funds to be used for a wider array of wellness programs or even non-medical expenses without penalty (especially after retirement age) periodically arise.

- Contribution Limit Adjustments: While annual inflation adjustments are standard, future legislation could push for more substantial increases to contribution limits to help individuals save more for escalating healthcare costs.

- Simplified Administration: Efforts to streamline HSA administration and reduce complexity for both account holders and employers are also often on the legislative agenda.

Beyond legislative changes, the increasing adoption of digital health solutions and personalized medicine could influence how HSA funds are utilized, potentially broadening the scope of what constitutes a “qualified medical expense.” As healthcare becomes more consumer-driven, HSAs are likely to remain a central tool for managing these evolving costs.

The future of HSAs appears robust, with a strong likelihood of continued relevance and potential enhancements. By staying informed about policy developments and adapting your strategy, you can ensure your 2026 Health Savings Account remains a powerful and flexible asset in your financial portfolio.

| Key Aspect | Brief Description |

|---|---|

| 2026 HSA Limits | Annual maximum contribution amounts for individuals and families, typically adjusted for inflation. |

| Eligibility | Must be covered by a High-Deductible Health Plan (HDHP) and not have other disqualifying coverage. |

| Triple Tax Advantage | Tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. |

| Strategic Use | Beyond immediate care, HSAs can serve as a long-term investment for retirement healthcare costs. |

Frequently Asked Questions About 2026 HSA Limits

While official 2026 HSA contribution limits will be released by the IRS later, they are generally expected to increase from 2025 due to inflation. Historically, both individual and family limits, along with catch-up contributions for those 55 and older, see slight upward adjustments each year.

To qualify for an HSA in 2026, you must be enrolled in a High-Deductible Health Plan (HDHP) that meets specific IRS criteria for minimum deductibles and maximum out-of-pocket expenses. You cannot be enrolled in Medicare, nor can you be claimed as a dependent on someone else’s tax return.

The triple tax advantage refers to three key benefits: tax-deductible contributions, tax-free growth on investments within the account, and tax-free withdrawals for qualified medical expenses. This makes HSAs a highly efficient vehicle for healthcare savings and retirement planning.

Before age 65, using HSA funds for non-qualified expenses incurs both ordinary income tax and a 20% penalty. After age 65, you can withdraw funds for any purpose without penalty, but non-qualified withdrawals will be subject to ordinary income tax, similar to a traditional IRA.

Yes, an HSA can be an excellent retirement savings tool, especially for healthcare costs. Its tax-free growth and tax-free withdrawals for medical expenses in retirement make it highly advantageous. Many individuals invest their HSA funds and let them grow for decades, using it as a dedicated healthcare endowment.

Conclusion

The 2026 Health Savings Account (HSA) limits represent a vital opportunity for individuals to strategically manage their healthcare finances and build substantial long-term wealth. By understanding the eligibility criteria, actively maximizing contributions, and leveraging the powerful triple tax advantage, you can transform your HSA into a cornerstone of your financial planning. Avoiding common pitfalls and staying informed about potential legislative changes will ensure your HSA remains an effective tool for both immediate medical needs and future retirement healthcare expenses. Embracing the full potential of your HSA in 2026 is a smart move toward greater financial security and peace of mind.