Student Loan Repayment 2026: A 4-Step Guide

Anúncios

Effectively managing student loan repayment in 2026 requires understanding federal and private loan distinctions, exploring available repayment plans, and strategically planning to achieve financial stability and debt freedom.

Anúncios

Navigating the landscape of student loan debt can feel overwhelming, especially with evolving regulations and economic shifts. For those facing their financial future in the coming years, understanding student loan repayment 2026 is paramount. This guide provides a clear, practical 4-step approach to help you confidently manage your student loans and pave the way for financial well-being.

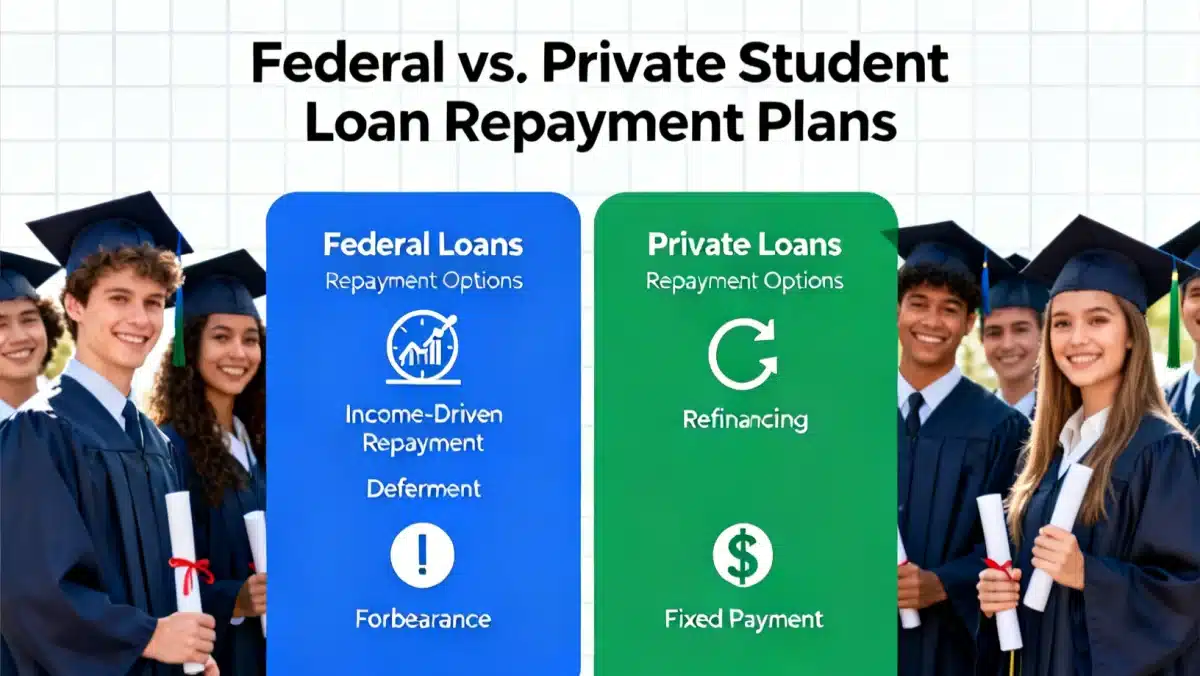

Step 1: Know Your Loans – Federal vs. Private in 2026

Before you can effectively plan your repayment strategy, you must first understand the type of student loans you hold. The distinction between federal and private student loans is crucial, as each comes with different terms, protections, and repayment options. In 2026, these differences remain foundational to your approach.

Federal student loans, issued by the U.S. Department of Education, typically offer more flexible repayment plans, including income-driven options, as well as opportunities for deferment, forbearance, and potential forgiveness programs. These loans are often more consumer-friendly due to their government backing and policy-driven structure. Private student loans, on the other hand, are offered by banks, credit unions, and other private lenders. While they can fill funding gaps, they generally have fewer borrower protections and less flexible repayment terms.

Identifying Your Loan Types

- Federal Loans: Check the National Student Loan Data System (NSLDS) which is accessible via the Federal Student Aid website. This portal provides a comprehensive overview of your federal loan history, including loan types, servicers, and current statuses.

- Private Loans: Review your credit report through one of the three major credit bureaus (Equifax, Experian, TransUnion). Private loans will be listed under the lender’s name, along with details of the loan amount and repayment status.

Knowing exactly what you owe and to whom is the critical first step. This clarity allows you to then explore the specific repayment plans applicable to your situation. Without this foundational knowledge, you might miss out on beneficial programs designed to ease your financial burden.

Step 2: Explore Federal Repayment Plans and Their 2026 Updates

For federal student loan borrowers, a variety of repayment plans exist, each designed to fit different financial situations. In 2026, while the core structures of these plans are expected to remain largely consistent, it’s wise to be aware of any potential legislative changes or updates that might impact their terms or eligibility.

Standard repayment plans typically amortize your loan over 10 years with fixed monthly payments. However, for many, this isn’t feasible, leading to the popularity of income-driven repayment (IDR) plans. These plans adjust your monthly payment based on your income and family size, often extending the repayment period and offering loan forgiveness after a certain number of years.

Key Federal Repayment Options

- SAVE Plan (formerly REPAYE): This income-driven plan often offers the lowest monthly payments, especially for low-income borrowers. Payments are capped at a percentage of your discretionary income and any unpaid interest may not accrue, preventing your balance from growing.

- PAYE (Pay As You Earn) & IBR (Income-Based Repayment): These plans also base payments on income and family size, with forgiveness after 20 or 25 years of qualifying payments. Eligibility for PAYE is generally stricter than IBR.

- Extended & Graduated Plans: These options offer lower initial payments that increase over time, or extend the repayment period up to 25 years, making monthly payments more manageable for some borrowers, though typically resulting in more interest paid over the life of the loan.

Understanding the nuances of each federal plan is essential. For instance, the SAVE plan, having been introduced recently, aims to be particularly generous for many borrowers. Regularly checking the Federal Student Aid website for the latest updates in 2026 will ensure you are informed about any modifications to these programs. This proactive approach can significantly impact your long-term financial health and ensure you’re on the most advantageous repayment path.

Step 3: Strategize Private Loan Management and Refinancing in 2026

Managing private student loans requires a different set of strategies compared to federal loans. Since private lenders offer fewer standardized protections, borrowers must be more proactive in seeking favorable terms or alternative solutions. In 2026, the private lending market will continue to offer options, but careful consideration is key.

Private loan terms are set by the lender and generally depend on your creditworthiness and that of any co-signer at the time of application. This means there’s less flexibility for income-based adjustments. However, refinancing remains a powerful tool for private loan borrowers, and sometimes even for federal loan borrowers willing to forgo federal protections for a lower interest rate.

Considering Private Loan Refinancing

- Lower Interest Rates: If your credit score has improved significantly since you took out your loans, or if interest rates have dropped, refinancing could secure a lower interest rate, reducing your total cost of borrowing.

- Simplified Payments: Consolidating multiple private loans into a single new loan can simplify your monthly payments and streamline your financial management.

- Changing Loan Terms: Refinancing can also allow you to adjust your repayment term, potentially lowering your monthly payment by extending the term, or paying off your loan faster by shortening it.

Before refinancing federal loans into a private loan, thoroughly weigh the loss of federal benefits, such as income-driven repayment, deferment, forbearance, and potential loan forgiveness. For private loans, however, refinancing can often be a straightforward decision if it results in better terms. Always compare offers from multiple lenders to find the most competitive rates and terms available in 2026 for your specific financial situation.

Anúncios

Step 4: Develop a Personalized Repayment Strategy and Budget

With a clear understanding of your loan types and available repayment options, the final step involves crafting a personalized repayment strategy and integrating it into your overall budget. This is where theory meets practice, ensuring your student loan payments are manageable and align with your broader financial goals in 2026.

A well-structured budget is the cornerstone of effective debt management. It allows you to see where your money is going, identify areas for savings, and ensure you have sufficient funds each month to cover your loan payments without undue stress. This step is about more than just making payments; it’s about optimizing your financial life around your debt.

Building Your Repayment Budget

- Assess Your Income and Expenses: Create a detailed overview of your monthly income and all fixed and variable expenses. This will highlight how much discretionary income you have available for loan payments.

- Prioritize Payments: Consider paying more than the minimum on loans with higher interest rates, often referred to as the “debt avalanche” method. Alternatively, the “debt snowball” method focuses on paying off the smallest loan first to build momentum.

- Automate Payments: Setting up automatic payments can help you avoid missed payments, which can incur late fees and negatively impact your credit score. Many lenders also offer a small interest rate reduction for auto-pay enrollment.

Regularly review and adjust your budget and repayment strategy. Life circumstances change, and your financial plan should be flexible enough to adapt. Whether it’s a promotion, a new expense, or a shift in market interest rates, staying agile will help maintain control over your student loan debt. This continuous monitoring is vital for achieving financial stability and ultimately, debt freedom.

Understanding Deferment and Forbearance in 2026

Even with the best repayment strategy, life can throw unexpected challenges your way. For federal student loan borrowers, deferment and forbearance options can provide temporary relief during periods of financial hardship. It’s important to understand the distinctions between these two options and when it’s appropriate to use them in 2026.

Deferment allows you to temporarily postpone your loan payments. During deferment, the government may pay the interest on subsidized federal loans, preventing your balance from growing. Common reasons for deferment include enrollment in school, unemployment, or economic hardship. Forbearance also allows you to temporarily stop or reduce your payments, but interest typically accrues on all types of federal loans during this period, potentially increasing your total debt.

When to Consider These Options

- Deferment: Ideal for situations where you meet specific eligibility criteria, such as returning to school at least half-time, experiencing unemployment, or serving in the military. It’s generally more beneficial than forbearance if you have subsidized loans, as interest won’t accrue.

- Forbearance: A broader option for those facing temporary financial difficulties not covered by deferment criteria, such as medical expenses, changes in employment, or other personal issues. Be mindful of interest accumulation during forbearance.

Both deferment and forbearance are temporary solutions, not long-term repayment strategies. They can provide a much-needed pause, but it’s crucial to understand their implications, especially regarding interest accrual. Always communicate with your loan servicer as soon as you anticipate difficulty in making payments to explore the best temporary relief options available to you in 2026.

Public Service Loan Forgiveness (PSLF) and Other Forgiveness Programs in 2026

For many federal student loan borrowers, the prospect of loan forgiveness can be a powerful motivator and a significant financial relief. Public Service Loan Forgiveness (PSLF) remains a cornerstone program for those dedicating their careers to public service. However, it’s essential to understand its specific requirements and potential updates in 2026.

PSLF forgives the remaining balance on Direct Loans after you have made 120 qualifying monthly payments while working full-time for a qualifying employer. This typically includes government organizations at any level (federal, state, local, or tribal) and not-for-profit organizations that are tax-exempt under Section 501(c)(3) of the Internal Revenue Code. The program has specific rules regarding loan types and payment plans, which must be strictly followed.

Key Aspects of PSLF and Other Forgiveness

- Qualifying Employment: Your employer must be a government organization or a 501(c)(3) non-profit. Volunteering or working for a for-profit organization, even if it provides public services, generally does not qualify.

- Eligible Loans: Only Direct Loans are eligible for PSLF. If you have FFEL Program loans or Perkins Loans, you may need to consolidate them into a Direct Consolidation Loan to qualify.

- Income-Driven Repayment: To maximize the benefit of PSLF, you generally need to be on an income-driven repayment plan, as this often results in lower monthly payments and a larger amount to be forgiven after 120 payments.

Beyond PSLF, other forgiveness or discharge options may be available, such as Teacher Loan Forgiveness, total and permanent disability discharge, or discharge in bankruptcy (though this is rare and difficult to obtain). Staying informed about these programs through the official Federal Student Aid website is crucial. Always keep meticulous records of your employment and payments to ensure you meet all requirements for any forgiveness program you pursue in 2026.

| Key Aspect | Brief Description |

|---|---|

| Loan Type Identification | Distinguish between federal and private loans to understand available options and protections. |

| Federal Repayment Plans | Explore income-driven plans (SAVE, PAYE, IBR) for flexible payments based on income. |

| Private Loan Strategy | Consider refinancing private loans for potentially lower interest rates or better terms. |

| Budgeting & Forgiveness | Develop a budget and explore PSLF or other forgiveness programs for federal loans. |

Frequently asked questions about student loan repayment in 2026

Federal student loans offer more borrower protections, such as income-driven repayment plans, deferment, forbearance, and potential forgiveness programs. Private loans, from banks, typically have fewer flexible options and depend more on credit scores for terms.

IDR plans, like the SAVE plan, adjust your monthly payment based on your income and family size. Payments are capped at a percentage of your discretionary income, and remaining balances may be forgiven after 20-25 years of qualifying payments, often preventing interest capitalization.

Refinancing private student loans can be beneficial if you can secure a lower interest rate or more favorable terms, especially if your credit has improved. It can reduce your total cost of borrowing or simplify payments by consolidating multiple loans.

PSLF forgives the remaining balance on Direct Loans after 120 qualifying payments made while working full-time for a government or eligible non-profit organization. It’s a significant benefit for those in public service careers, but strict adherence to rules is necessary.

Start by assessing your income and all expenses to determine discretionary funds. Prioritize higher-interest loans, consider automating payments to avoid late fees, and regularly review your budget to adapt to changing financial circumstances for optimal management.

Conclusion

Successfully navigating your student loan repayment in 2026 is an achievable goal with a structured approach. By understanding your loan types, exploring federal and private options, strategically planning your payments, and staying informed about potential forgiveness programs, you can take control of your financial future. Proactive research, communication with your loan servicers, and diligent budgeting are your most powerful tools in transforming student debt into a manageable part of your financial journey. Embrace these steps to move confidently towards financial freedom and stability.