Maximize 2025 HSA Benefits: $4,150 Tax-Free Growth Guide

Anúncios

Maximize Your 2025 Health Savings Account (HSA) Benefits: A Guide to $4,150 in Tax-Free Growth empowers individuals to strategically use their HSA for substantial tax advantages and long-term healthcare savings.

Anúncios

Are you ready to truly Maximize Your 2025 Health Savings Account (HSA) Benefits: A Guide to $4,150 in Tax-Free Growth? For many Americans, the HSA is far more than just a savings account for medical expenses; it’s a powerful, triple-tax-advantaged investment vehicle that can secure your financial future, especially as healthcare costs continue to rise. Understanding the nuances of HSA contributions, eligible expenses, and investment opportunities is crucial to leveraging its full potential. This guide will walk you through the essential strategies to make your HSA work harder for you in 2025, potentially growing your wealth tax-free.

Understanding the 2025 HSA Landscape and Contribution Limits

The Health Savings Account (HSA) remains a cornerstone of smart financial planning for those enrolled in a high-deductible health plan (HDHP). In 2025, understanding the updated contribution limits is your first step toward maximizing its benefits. These limits are adjusted annually by the IRS to account for inflation, providing an opportunity for individuals and families to save even more.

For 2025, the IRS has set new thresholds, allowing individuals to contribute a significant amount towards their healthcare savings. This isn’t just about covering immediate medical costs; it’s about building a robust fund for future health needs, including those in retirement. The power of the HSA lies in its flexibility and its unique tax advantages.

Key Contribution Figures for 2025

Staying informed about the exact numbers is critical. Exceeding these limits can lead to penalties, while underutilizing them means missing out on substantial tax-free growth potential. These figures represent the maximum you can contribute from all sources, including employer contributions and your own.

- Individual Contribution Limit: For self-only HDHP coverage, the maximum contribution is set to increase, allowing for greater personal savings.

- Family Contribution Limit: For family HDHP coverage, this limit is substantially higher, reflecting the greater potential healthcare needs of multiple individuals.

- Catch-Up Contributions: Individuals aged 55 and over can make additional catch-up contributions, further boosting their savings.

These limits are not merely suggestions; they are the legal boundaries within which you can operate to enjoy the full tax benefits of your HSA. Planning your contributions strategically throughout the year can help you reach these maximums without financial strain, ensuring you fully capitalize on this powerful savings tool. It’s important to remember that these limits apply to the calendar year, so front-loading contributions early can accelerate your investment growth.

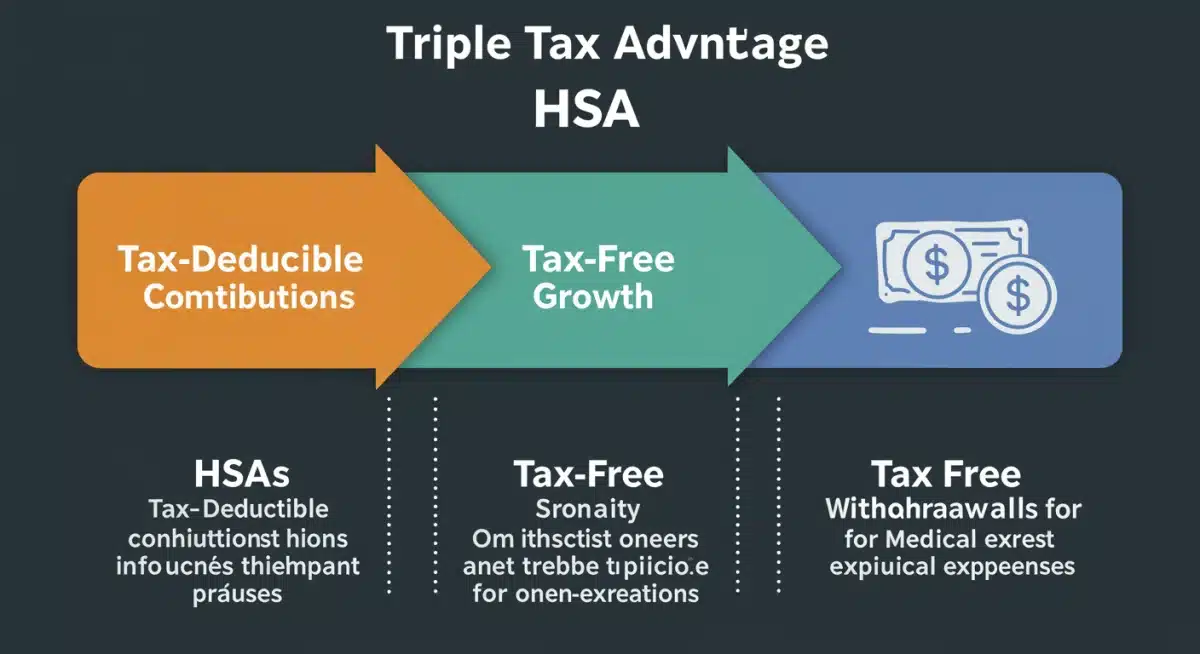

The Triple Tax Advantage: Why HSAs are Unmatched

Beyond just saving for healthcare, the HSA offers a unique combination of tax benefits often referred to as the “triple tax advantage.” This makes it one of the most powerful savings and investment vehicles available today, especially when compared to other retirement or investment accounts. Understanding these three pillars is key to appreciating the true value of your HSA.

No other account offers this specific trifecta of tax benefits, making the HSA an essential component of a comprehensive financial plan. When you contribute, grow, and withdraw funds from an HSA for qualified medical expenses, you effectively bypass taxes at every stage. This can lead to significant savings over the long term, far beyond what traditional savings accounts or even 401(k)s might offer for medical costs.

Breaking Down the Three Pillars

Each element of the triple tax advantage contributes to the HSA’s exceptional power. First, your contributions are tax-deductible, meaning they reduce your taxable income in the year you make them. This is an immediate benefit that lowers your current tax burden.

- Tax-Deductible Contributions: Money you put into your HSA is deducted from your gross income, lowering your taxable income for the year. This is true whether you contribute directly or through payroll deductions.

- Tax-Free Growth: Once funds are in your HSA, they can be invested, and any earnings, dividends, or capital gains grow tax-free. This compounding growth is a significant advantage, particularly over many years.

- Tax-Free Withdrawals: When you use your HSA funds for qualified medical expenses, the withdrawals are entirely tax-free. This includes a wide range of expenses, from doctor visits and prescriptions to dental care and vision.

This combination creates a highly efficient system for healthcare savings. Imagine contributing pre-tax dollars, watching those dollars grow without being taxed on the gains, and then withdrawing them tax-free for medical needs. This unparalleled advantage is what makes the HSA a critical tool for financial security, especially as you age and healthcare needs potentially increase.

Investing Your HSA for Maximum Tax-Free Growth

One of the most overlooked aspects of an HSA is its potential as an investment vehicle. Many individuals treat their HSA like a checking account, using it only for immediate medical expenses. However, for those who can afford to pay for current medical costs out-of-pocket, investing their HSA funds can lead to substantial long-term growth, reaching that impressive tax-free increase.

The beauty of investing your HSA lies in the tax-free growth. Over decades, even modest investments can compound significantly, turning a relatively small initial contribution into a substantial nest egg for future healthcare expenses in retirement. This strategy requires a long-term perspective and a willingness to let your funds grow.

Anúncios

Choosing the Right Investment Strategy

Selecting an appropriate investment strategy for your HSA is similar to planning for any other long-term investment. Your risk tolerance, time horizon, and financial goals should all play a role in your decisions. Most HSA providers offer a range of investment options, from conservative to aggressive.

- Diversification: Spread your investments across various asset classes, such as stocks, bonds, and mutual funds, to mitigate risk.

- Low-Cost Funds: Opt for index funds or exchange-traded funds (ETFs) with low expense ratios to maximize your net returns over time.

- Long-Term Horizon: Since healthcare costs are likely to be a significant expense in retirement, consider a growth-oriented strategy if you are many years away from needing the funds.

Regularly review your HSA investment portfolio to ensure it aligns with your financial objectives and market conditions. Rebalancing periodically can help maintain your desired asset allocation. By treating your HSA as a serious investment account, you can unlock its full potential for tax-free growth, building a significant reserve for your future health needs.

Eligible Expenses and Strategic Withdrawals

Understanding what constitutes an “eligible medical expense” is fundamental to maintaining the tax-free status of your HSA withdrawals. The IRS provides clear guidelines, and adhering to them ensures you avoid potential taxes and penalties. This knowledge allows for strategic planning around when and how to use your HSA funds.

While many common medical costs are covered, there are also less obvious expenses that qualify, which can expand the utility of your HSA. Keeping detailed records of all medical expenses, even those you pay out-of-pocket, is a smart practice. This allows you to reimburse yourself tax-free from your HSA at any point in the future, even years later.

Common and Less Obvious Qualified Expenses

From routine check-ups to specialized treatments, a wide array of expenses can be paid for with HSA funds. It’s not just about doctor visits; it encompasses various aspects of health and wellness that contribute to your overall well-being.

- Medical and Dental Care: Doctor visits, hospital stays, prescriptions, dental treatments, and vision care (glasses, contacts).

- Preventive Care: Many preventive services, even if your HDHP doesn’t cover them entirely, can be paid from your HSA.

- Long-Term Care Premiums: A portion of long-term care insurance premiums can be paid tax-free from your HSA, based on age-adjusted limits.

- Over-the-Counter Medications: Many OTC items are now eligible, making everyday health purchases more advantageous.

A powerful strategy is to pay for current medical expenses out-of-pocket and allow your HSA funds to continue growing tax-free. Then, in retirement, you can reimburse yourself for all those past qualified expenses, effectively creating a tax-free income stream. This requires meticulous record-keeping, but the long-term financial benefits can be substantial, cementing the HSA’s role as a potent retirement planning tool.

HSA in Retirement: A Powerful Financial Asset

The true power of the HSA often becomes most apparent in retirement. For many, healthcare costs are among the largest and most unpredictable expenses during their golden years. An HSA, strategically grown over decades, can serve as an invaluable financial asset, providing a dedicated, tax-free fund for these inevitable costs.

Unlike a 401(k) or IRA, where withdrawals in retirement are typically taxed (unless it’s a Roth), qualified medical expense withdrawals from an HSA remain tax-free at any age. This makes the HSA an ideal complement to other retirement accounts, offering a unique layer of financial security specifically for health-related expenditures.

Integrating HSA into Your Retirement Plan

Thinking of your HSA as a long-term investment account for retirement healthcare costs can significantly alter your financial outlook. It can alleviate concerns about medical bills, allowing you to enjoy your retirement years with greater peace of mind.

- Covering Medicare Premiums: Once enrolled in Medicare, HSA funds can be used to pay for Medicare Part B, Part D, and Medicare Advantage plan premiums, though not Medigap premiums.

- Long-Term Care: HSA funds can cover a wide range of long-term care services, which can be incredibly expensive and often not fully covered by Medicare.

- Non-Medical Withdrawals Post-65: After age 65, you can withdraw HSA funds for any reason without penalty. While these withdrawals will be taxed as ordinary income if not used for qualified medical expenses, this flexibility provides an additional retirement income source if needed.

By consistently contributing the maximum allowable amount, investing wisely, and preserving your funds for future needs, your HSA can evolve into a robust financial safety net for retirement healthcare. This proactive approach ensures that you are well-prepared for the escalating costs of medical care, allowing your other retirement savings to be used for living expenses and leisure.

Advanced Strategies and Common Pitfalls to Avoid

While the fundamental principles of HSAs are straightforward, there are advanced strategies that can further enhance your benefits, as well as common pitfalls that can diminish them. Navigating these complexities effectively ensures you fully capitalize on your HSA’s potential.

One advanced strategy involves paying for current medical expenses out-of-pocket and meticulously tracking them. This allows your HSA investments to grow untouched and tax-free for decades. You can then reimburse yourself for these past expenses at any point in the future, creating a significant tax-free withdrawal opportunity when you need it most, such as in retirement.

Smart Moves and Things to Watch Out For

Being proactive and informed about your HSA management can make a substantial difference in its long-term value. From contribution timing to investment choices, every decision can impact your overall financial health.

- Maximizing Contributions Early: Contributing the maximum at the beginning of the year allows your investments more time to grow tax-free.

- Avoid Non-Qualified Withdrawals: Before age 65, non-qualified withdrawals are subject to ordinary income tax plus a 20% penalty. After 65, the penalty is waived, but income taxes still apply.

- Consolidate HSAs: If you’ve had multiple HSAs with different employers, consider consolidating them into a single account with robust investment options and lower fees.

- Keep Meticulous Records: Essential for reimbursing yourself for past medical expenses tax-free, especially if you defer withdrawals for many years.

Another often-overlooked strategy is using your HSA as an emergency fund specifically for medical emergencies. While it’s ideal to let it grow, having a readily accessible fund for unexpected high-deductible costs can prevent you from dipping into other savings. By understanding these advanced tactics and avoiding common mistakes, you can ensure your HSA truly serves its purpose as a powerful tool for both current and future financial well-being.

| Key Aspect | Brief Description |

|---|---|

| 2025 Contribution Limits | IRS-adjusted maximums for individuals and families, crucial for maximizing tax-advantaged savings. |

| Triple Tax Advantage | Contributions are tax-deductible, growth is tax-free, and qualified withdrawals are tax-free. |

| Investment Potential | HSA funds can be invested for long-term, tax-free growth, acting as a retirement savings vehicle. |

| Retirement Security | HSA funds provide a tax-free source for healthcare costs in retirement, including Medicare premiums. |

Frequently Asked Questions About HSAs

The primary benefits include pre-tax contributions, tax-free growth on investments, and tax-free withdrawals for qualified medical expenses. This triple tax advantage makes it a powerful tool for saving for current and future healthcare costs, including those in retirement.

To be eligible, you must be enrolled in a high-deductible health plan (HDHP), not be covered by any other health insurance (with some exceptions), not be enrolled in Medicare, and not be claimed as a dependent on someone else’s tax return.

Yes, you can invest HSA funds in various options like mutual funds or ETFs, offered by your HSA provider. Any earnings from these investments grow tax-free, and when withdrawn for qualified medical expenses, they remain tax-free.

Unused HSA funds roll over year after year and never expire. After age 65, you can withdraw funds for any reason without penalty. However, non-medical withdrawals will be taxed as ordinary income, similar to a traditional IRA.

Yes, if you use HSA funds for non-qualified expenses before age 65, the amount withdrawn will be subject to ordinary income tax plus a 20% penalty. After age 65, the penalty is waived, but income tax still applies.

Conclusion

The Health Savings Account truly stands out as an exceptional financial tool, offering unparalleled tax advantages for healthcare savings and long-term investment. By understanding and actively engaging with the 2025 contribution limits, leveraging the triple tax advantage, and making strategic investment choices, individuals can significantly maximize their 2025 Health Savings Account (HSA) benefits. This proactive approach not only helps manage current medical costs but also builds a robust, tax-free fund for future healthcare needs, especially in retirement. Embracing the HSA as more than just a spending account, but as a critical component of your financial future, is a decision that can yield substantial rewards and provide lasting peace of mind.