Maximize Your HSA in 2026: Tax-Free Growth Strategies

Anúncios

To strategically maximize Your Health Savings Account (HSA) in 2026: 5 Insider Strategies for Tax-Free Growth, focus on consistent contributions, early investment, and understanding withdrawal rules to leverage its unparalleled tax benefits for future healthcare costs.

Anúncios

Are you ready to truly maximize your Health Savings Account (HSA) in 2026: 5 Insider Strategies for Tax-Free Growth? This powerful financial tool offers a unique opportunity to save for healthcare expenses with incredible tax advantages. Far more than just a savings account, an HSA can be a cornerstone of your long-term financial planning, providing a triple tax benefit that is hard to match. By understanding and implementing smart strategies, you can transform your HSA from a simple health fund into a significant investment vehicle.

Understanding the HSA Advantage in 2026

The Health Savings Account (HSA) remains one of the most powerful and often underutilized financial tools available to eligible Americans in 2026. It’s not just for current medical costs; it’s a versatile savings and investment vehicle designed to cover future healthcare expenses. Its unique triple tax advantage sets it apart from other retirement or savings accounts, making it an essential component of a robust financial strategy.

To qualify for an HSA, you must be enrolled in a High Deductible Health Plan (HDHP) and not be enrolled in Medicare. The IRS sets annual contribution limits, which tend to increase each year, reflecting inflation and healthcare cost trends. For 2026, these limits are expected to continue their upward trajectory, allowing for even greater tax-advantaged savings. Understanding these foundational aspects is the first step toward effectively maximizing your HSA.

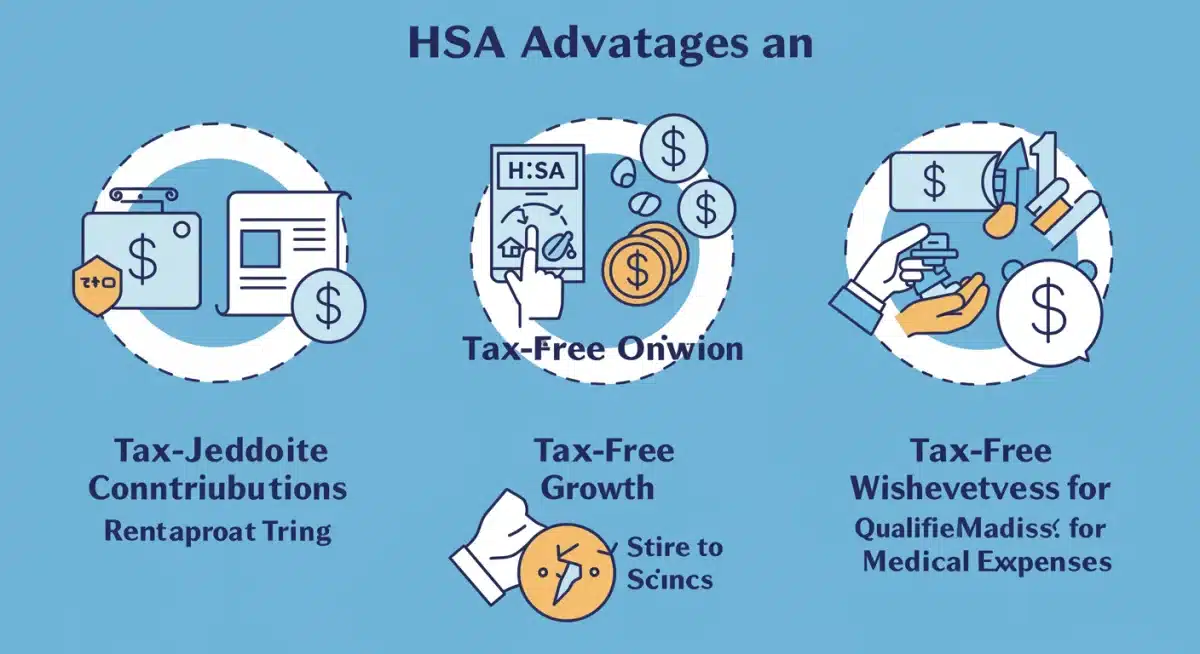

The Triple Tax Benefit Explained

The core appeal of an HSA lies in its unparalleled tax benefits. These advantages create a powerful incentive for consistent contributions and long-term investment, significantly boosting your savings potential.

- Tax-Deductible Contributions: Money you contribute to your HSA is tax-deductible, reducing your taxable income in the year you contribute. This is an immediate saving on your federal income taxes, and often on state taxes as well.

- Tax-Free Growth: Any investment gains within your HSA grow tax-free. This means you won’t pay taxes on dividends, interest, or capital gains as long as the money remains in the account. This compounding effect over decades can lead to substantial wealth accumulation.

- Tax-Free Withdrawals: When you withdraw funds from your HSA for qualified medical expenses, those withdrawals are completely tax-free. This includes a wide range of expenses, from doctor visits and prescriptions to dental care and even long-term care insurance premiums.

Eligibility and Contribution Limits for 2026

Eligibility for an HSA is tied to your health insurance plan. In 2026, you must be covered by an HDHP, generally defined by a minimum deductible and a maximum out-of-pocket limit. These thresholds are adjusted annually by the IRS. It’s crucial to verify that your health plan meets these specific requirements to ensure your eligibility. Furthermore, the IRS also sets the maximum amount you can contribute to an HSA each year, with additional catch-up contributions allowed for individuals aged 55 and over. Staying informed about these limits is vital for maximizing your savings.

Beyond the immediate tax benefits, the flexibility of an HSA is another key advantage. Unlike Flexible Spending Accounts (FSAs), HSA funds roll over year after year, never expiring. This means you can save diligently without fear of losing your contributions, making it an ideal vehicle for both short-term healthcare needs and long-term planning. The ability to invest these funds further amplifies their growth potential, transforming them into a significant asset for retirement and beyond. Understanding these aspects is crucial for anyone looking to truly leverage their HSA.

Strategy 1: Maximize Your Contributions Annually

One of the most straightforward yet impactful ways to maximize your Health Savings Account (HSA) in 2026 is to contribute the maximum allowed amount each year. This strategy takes full advantage of the triple tax benefits and sets the stage for significant long-term growth. Many individuals underutilize their HSA, contributing only enough to cover immediate medical expenses. However, viewing your HSA as an investment vehicle rather than just a spending account changes the game entirely.

The IRS sets annual contribution limits, which typically see slight increases each year to account for inflation. For 2026, it’s expected these limits will be higher than previous years, offering more room for tax-advantaged savings. By consistently hitting these maximums, especially if you qualify for catch-up contributions (for those 55 and older), you accelerate the growth of your account substantially. This disciplined approach ensures you’re fully leveraging the tax deductions available to you, immediately reducing your taxable income.

Understanding 2026 Contribution Limits

It’s critical to stay updated on the specific HSA contribution limits for 2026. These figures are usually announced by the IRS in the latter half of the preceding year. Employers often facilitate contributions directly from payroll, which means these contributions are made pre-tax, adding another layer of tax savings by avoiding FICA taxes (Social Security and Medicare). If you contribute after-tax, you can still deduct these contributions when you file your income taxes.

- Individual Coverage: Expected to be higher than previous years, allowing a substantial amount for single filers.

- Family Coverage: A significantly larger limit for those covering themselves and at least one other family member under an HDHP.

- Catch-Up Contributions: An additional contribution allowed for individuals aged 55 and over, further boosting their savings potential as they approach retirement.

The Power of Consistent Maximum Contributions

Consistent maximum contributions, year after year, are the bedrock of a powerful HSA strategy. This approach not only provides immediate tax relief but also fuels the tax-free growth of your investments. Over time, even small annual increases in contribution limits, when compounded with tax-free growth, can lead to a substantial balance. Think of your HSA as a self-funded healthcare endowment, growing steadily to cover future medical costs, especially in retirement when healthcare expenses often increase.

Many HSAs offer investment options, allowing your contributions to grow beyond simple savings. By maximizing contributions, you ensure more capital is available to be invested. This strategy is particularly effective for younger individuals who have many years for their investments to compound. Even if you don’t use the funds immediately for medical expenses, the ability to invest them and let them grow tax-free is an unparalleled advantage. Therefore, making it a priority to contribute the maximum each year is a fundamental step towards long-term financial health and medical expense coverage.

Anúncios

Strategy 2: Invest Your HSA Funds Early and Aggressively

Simply contributing to your HSA is a good start, but to truly maximize your Health Savings Account (HSA) for tax-free growth in 2026, you must invest those funds. Many HSA account holders leave their money in cash, missing out on the significant growth potential offered by the market. An HSA is not just a savings account; it’s an investment vehicle with unique tax advantages that can build substantial wealth over time, particularly for future healthcare costs.

The earlier you start investing your HSA funds, the more time compounding has to work its magic. Given the tax-free growth within an HSA, every dollar earned through investments is another dollar that doesn’t get taxed, amplifying your returns. For individuals with a long time horizon until retirement, an aggressive investment strategy, focusing on growth-oriented assets like stocks or equity mutual funds, can yield impressive results. This approach shifts your HSA from a mere spending account to a powerful wealth-building tool.

Choosing the Right Investment Options

Most HSA providers offer a range of investment options, similar to those found in 401(k)s or IRAs. These typically include mutual funds, exchange-traded funds (ETFs), and sometimes even individual stocks. When selecting investments, consider your risk tolerance and your time horizon. For those many years away from retirement, a more aggressive portfolio might be appropriate, as short-term market fluctuations are less impactful over the long run.

- Diversified Equity Funds: These funds offer broad market exposure and are suitable for long-term growth.

- Target-Date Funds: A convenient option that automatically adjusts its asset allocation as you approach a specific retirement year.

- Low-Cost Index Funds: These provide broad market exposure with minimal fees, maximizing your net returns.

Rebalancing Your Portfolio and Managing Risk

Like any investment portfolio, your HSA investments should be periodically reviewed and rebalanced. As you get closer to needing the funds for major healthcare expenses, or as you approach retirement, you might consider shifting towards more conservative investments to protect your accumulated gains. This gradual de-risking ensures that your funds are available when you need them, without being overly exposed to market volatility.

It’s also important to be aware of any fees associated with your HSA investments. Some providers charge administrative fees or have higher expense ratios on their investment options. Minimizing these costs can significantly impact your long-term returns. By actively managing your HSA investments and choosing low-cost, diversified funds, you can significantly enhance its tax-free growth potential, making it a cornerstone of your financial security for future healthcare needs.

Strategy 3: Pay for Current Medical Expenses Out-of-Pocket

This strategy might seem counterintuitive at first, but it is a powerful insider tip to maximize your Health Savings Account (HSA) for tax-free growth in 2026. Instead of immediately drawing from your HSA for current medical expenses, consider paying for those qualified costs out-of-pocket if you have the available cash flow. The key benefit here is that it allows your HSA funds to remain invested and continue growing tax-free for a longer period.

The beauty of an HSA is that there’s no deadline for reimbursement of qualified medical expenses. You can pay for a medical bill today with your regular checking account and then, years or even decades later, reimburse yourself from your HSA for that exact expense, completely tax-free. This approach essentially turns your HSA into an even more powerful investment vehicle, as every dollar you leave invested has more time to compound and grow.

Tracking Qualified Medical Expenses

To successfully implement this strategy, meticulous record-keeping is paramount. You need to keep detailed records of all qualified medical expenses that you pay for out-of-pocket. This includes receipts, bills, and explanations of benefits (EOBs) from your insurance company. These records will be crucial if you ever need to justify a tax-free reimbursement from your HSA in the future.

- Maintain a Digital Folder: Scan and save all medical receipts and EOBs in a dedicated digital folder for easy access and organization.

- Use a Spreadsheet: Create a simple spreadsheet to log each expense, including the date, amount, and a brief description.

- Consult IRS Publication 502: Regularly review IRS Publication 502 for a comprehensive list of what constitutes a qualified medical expense.

The Long-Term Payout of Delayed Reimbursement

Imagine paying a $500 medical bill today with your own money. If you leave that $500 in your HSA and it grows at an average of 7% annually, in 20 years, that $500 could be worth nearly $2,000. When you finally decide to reimburse yourself for the original $500, the extra $1,500 in growth is completely tax-free. This delayed reimbursement strategy allows you to turn ordinary medical expenses into a significant source of tax-free income in retirement.

This strategy is particularly beneficial for those who are younger and have a longer investment horizon. By front-loading your HSA with invested funds and paying for current expenses out-of-pocket, you maximize the compounding effect. It’s a strategic move to treat your HSA not just as a spending account but as a long-term retirement savings vehicle specifically earmarked for healthcare. When managed correctly, this approach can significantly boost your overall financial health and provide a substantial tax-free nest egg for future medical needs.

Strategy 4: Leverage Your HSA as a Retirement Account

While primarily designed for healthcare expenses, an often-overlooked strategy to maximize your Health Savings Account (HSA) in 2026 is to treat it as a supplemental retirement account. After age 65, the rules governing HSA withdrawals become even more flexible, allowing you to use the funds for any purpose without penalty, although non-medical withdrawals will be taxed as ordinary income.

This dual function makes the HSA incredibly powerful. During your working years, you benefit from the tax deductions on contributions, tax-free growth, and tax-free withdrawals for medical expenses. However, once you reach retirement age, your HSA essentially transforms into a traditional IRA, but with the added benefit of tax-free withdrawals if used for qualified medical expenses. This flexibility provides a crucial safety net for healthcare costs in retirement, which can be substantial.

HSA vs. Other Retirement Accounts

Comparing an HSA to other popular retirement vehicles highlights its unique advantages. While 401(k)s and IRAs offer tax-deferred growth, their withdrawals in retirement are almost always taxed. An HSA, however, offers the potential for completely tax-free withdrawals if used for medical expenses, even in retirement. This makes it a superior option for covering what often becomes a significant expense category for retirees.

- 401(k)/IRA: Tax-deferred growth, but withdrawals are taxed in retirement.

- Roth IRA: After-tax contributions, tax-free growth and withdrawals in retirement, but no upfront tax deduction.

- HSA: Triple tax advantage – deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses at any age, or taxed as ordinary income for non-medical withdrawals after 65.

Planning for Healthcare in Retirement

Healthcare costs are a major concern for many retirees. Medicare premiums, deductibles, co-pays, and services not covered by Medicare (like dental, vision, and hearing aids) can quickly add up. A well-funded HSA can cover these expenses without dipping into your other retirement savings, preserving your taxable income for discretionary spending.

By intentionally contributing and investing in your HSA for the long haul, you’re not just saving for a rainy day; you’re building a dedicated, tax-advantaged fund specifically for your future health. This strategic approach ensures that you have the financial resources to maintain your health and quality of life throughout retirement, significantly easing financial stress. The HSA truly stands out as a versatile and essential tool for comprehensive retirement planning, offering unparalleled benefits for both health and wealth.

Strategy 5: Understand and Maximize Qualified Medical Expenses

To fully maximize your Health Savings Account (HSA) in 2026, it’s essential to have a comprehensive understanding of what constitutes a qualified medical expense. The IRS definition is surprisingly broad, extending far beyond typical doctor visits and prescription medications. By being aware of the full scope of eligible expenses, you can ensure that you are either getting tax-free reimbursements for past out-of-pocket costs or making tax-free withdrawals for current needs.

Many people only think of their HSA for routine medical care. However, it can cover a wide array of services and products that contribute to your health and well-being. Knowing these details allows you to confidently use your HSA funds without incurring taxes or penalties. This knowledge also supports the strategy of paying out-of-pocket now and reimbursing yourself later, as you’ll have a clear record of eligible expenses.

Broad Range of Eligible Healthcare Costs

The list of qualified medical expenses is extensive and includes many items you might not initially consider. This broad eligibility makes the HSA an incredibly flexible tool for managing healthcare costs across your lifespan. From preventative care to specialized treatments, your HSA can be a valuable resource.

- Preventative Care: Includes annual physicals, screenings, and vaccinations, often covered before meeting your deductible.

- Dental and Vision Care: Expenses for exams, cleanings, braces, glasses, contact lenses, and even laser eye surgery are typically covered.

- Mental Health Services: Therapy sessions, counseling, and psychiatric care are generally eligible expenses.

- Prescription Medications and Over-the-Counter Drugs: Prescribed medications are covered, and many over-the-counter drugs are also eligible if prescribed by a doctor.

- Long-Term Care Insurance Premiums: A portion of these premiums can be paid with HSA funds, offering significant tax advantages for future care.

Keeping Meticulous Records for Reimbursement

As mentioned in Strategy 3, maintaining detailed records of all qualified medical expenses is non-negotiable. If you plan to reimburse yourself years down the line, these records will be your proof that the withdrawals are for legitimate medical costs and thus tax-free. The IRS does not require you to submit these records with your tax return, but you must be able to provide them if audited.

This includes not only receipts from healthcare providers but also documentation for medical mileage, medical conferences, and even certain home modifications for medical care. By diligently tracking every eligible expense, you ensure that you can access your HSA funds tax-free when needed, making it a highly efficient and effective tool for managing healthcare finances. This strategic awareness of what qualifies as a medical expense is critical for maximizing both the utility and the tax benefits of your HSA.

| Key Strategy | Brief Description |

|---|---|

| Maximize Contributions | Contribute the maximum allowable amount annually to fully leverage tax deductions and fuel growth. |

| Invest Funds Aggressively | Move funds beyond cash into growth-oriented investments early for compounded tax-free returns. |

| Pay Out-of-Pocket | Cover current medical costs with personal funds to allow HSA investments to grow longer, then reimburse tax-free later. |

| Utilize as Retirement Account | Leverage the HSA’s flexibility after age 65 for penalty-free withdrawals, functioning like a supplemental retirement fund. |

Frequently Asked Questions About HSAs in 2026

In 2026, an HSA offers a triple tax advantage: contributions are tax-deductible, investment earnings grow tax-free, and withdrawals for qualified medical expenses are also tax-free. This combination makes it a highly efficient savings and investment vehicle for healthcare costs.

Yes, you can use your HSA for non-medical expenses, but with a caveat. Before age 65, such withdrawals are subject to ordinary income tax and a 20% penalty. After age 65, non-medical withdrawals are taxed as ordinary income but without the penalty, similar to a traditional IRA.

Your HSA funds are portable and belong to you, regardless of job changes or switching health plans. You can take your HSA with you, continue to contribute if eligible with a new HDHP, or let the existing funds grow and use them for future qualified medical expenses.

Yes, like any investment, HSA funds invested in the market carry inherent risks, including the potential loss of principal. However, with a long-term perspective and diversified investments, the potential for tax-free growth often outweighs these risks, especially for younger individuals.

To keep records for future HSA reimbursements, save all receipts, Explanation of Benefits (EOBs), and medical bills in a digital or physical folder. A simple spreadsheet tracking dates, amounts, and descriptions can also be very helpful for organization and easy retrieval if needed.

Conclusion

Successfully maximizing your Health Savings Account (HSA) in 2026 goes beyond simply using it for immediate medical bills. By adopting these five insider strategies – consistently maximizing contributions, investing funds aggressively from the outset, strategically paying for current expenses out-of-pocket, leveraging it as a robust retirement account, and comprehensively understanding qualified medical expenses – you can unlock the full potential of this powerful financial tool. The HSA’s triple tax advantage provides an unparalleled opportunity for tax-free growth, making it an indispensable asset for both your current and future financial well-being. Embrace these strategies to transform your HSA into a cornerstone of your long-term financial security, ensuring you are well-prepared for healthcare costs now and in retirement.